- Understanding the Challenges

- Income Verification

- Job Stability

- Credit History

- Exploring the Options

- FHA Loans

- Question-answer:

- Can a contract employee qualify for a home loan?

- What are the requirements for a contract employee to get a home loan?

- Are there any specific challenges that contract employees may face when applying for a home loan?

- What can contract employees do to improve their chances of getting a home loan?

- Are there any alternative options for contract employees who are unable to qualify for a traditional home loan?

When it comes to buying a home, many people assume that being a contract employee automatically disqualifies them from obtaining a home loan. However, this is not always the case. While it may be more challenging for contract employees to secure a mortgage compared to those with a traditional employment status, there are still possibilities to explore.

Understanding the Challenges

Contract employees often face additional hurdles when it comes to getting a home loan. Lenders typically prefer borrowers with a stable income and a long-term employment history. Contract employees, on the other hand, may have fluctuating income and shorter employment terms, making them appear riskier to lenders.

However, it’s important to note that not all lenders have the same strict criteria. Some lenders are more flexible and willing to work with contract employees to help them achieve their dream of homeownership.

Building a Strong Case

If you’re a contract employee and want to increase your chances of getting a home loan, there are several steps you can take. First, it’s crucial to have a solid financial track record. This includes maintaining a good credit score, paying off debts, and saving for a down payment.

Additionally, having a long-term contract or a history of consistent contract work can help demonstrate your stability and reliability to lenders. Providing documentation of your income, such as tax returns and bank statements, can also strengthen your case.

Exploring Alternative Options

If traditional lenders are hesitant to approve your home loan application, don’t lose hope. There are alternative options available, such as working with specialized lenders who cater to contract employees or considering government-backed loan programs.

Government-backed loan programs, such as FHA loans, may have more lenient requirements and can be a viable option for contract employees. These programs often have lower down payment requirements and more flexible income guidelines.

Ultimately, while being a contract employee may present some challenges, it doesn’t mean you can’t get a home loan. By understanding the possibilities and taking the necessary steps to strengthen your case, you can increase your chances of securing a mortgage and achieving your homeownership goals.

Understanding the Challenges

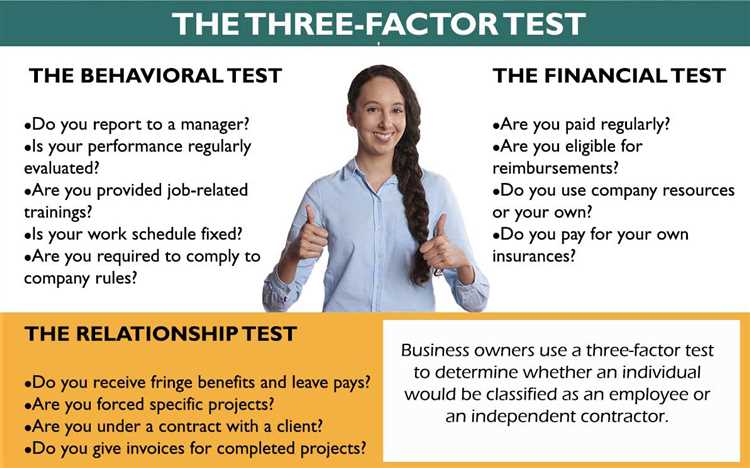

When it comes to getting a home loan as a contract employee, there are several challenges that you may face. These challenges can make it more difficult for you to qualify for a loan and may require you to take additional steps to prove your eligibility.

One of the main challenges is income verification. Unlike traditional employees who receive a regular paycheck, contract employees often have fluctuating income. Lenders may be hesitant to approve a loan if they cannot verify a stable income source. You may need to provide additional documentation, such as tax returns or contracts, to prove your income stability.

Another challenge is job stability. Contract employees typically do not have the same job security as traditional employees. Lenders may be concerned about the stability of your employment and may require you to have a longer work history or a higher level of savings to compensate for the potential income fluctuations.

Credit history is also an important factor that lenders consider when approving a home loan. Contract employees may have a harder time establishing a strong credit history, especially if they have not been working in the same field for a long time. It is important to maintain a good credit score and demonstrate responsible financial behavior to increase your chances of loan approval.

Overall, it is important for contract employees to understand the challenges they may face when applying for a home loan. By being prepared and taking steps to address these challenges, you can increase your chances of qualifying for a loan and achieving your dream of homeownership.

Income Verification

When it comes to getting a home loan as a contract employee, one of the main challenges you may face is income verification. Unlike traditional employees who receive a steady paycheck from an employer, contract employees often have fluctuating income.

During the loan application process, lenders will typically require proof of income to assess your ability to repay the loan. This can be more challenging for contract employees, as their income may not be as easily verifiable as that of a salaried employee.

However, there are still options available for contract employees to verify their income. One option is to provide copies of your contracts or agreements with clients, which can demonstrate a consistent stream of income. You may also be asked to provide bank statements showing regular deposits from your clients.

Another option is to provide tax returns for the past two years. This can help lenders assess your income stability and consistency over time. It is important to accurately report your income on your tax returns to ensure that it aligns with the income you are claiming for the loan application.

Additionally, some lenders may consider alternative forms of income verification for contract employees. This can include providing letters of recommendation from clients or colleagues, or providing proof of a long-term contract with a client.

It is important to note that each lender may have different requirements and criteria for income verification. It is advisable to consult with multiple lenders to explore your options and find a lender who is willing to work with contract employees.

Overall, while income verification can be a challenge for contract employees, it is not impossible to get a home loan. By providing the necessary documentation and working with a lender who understands the unique circumstances of contract employment, you can increase your chances of securing a home loan.

Job Stability

When it comes to getting a home loan as a contract employee, one of the key factors that lenders consider is job stability. Lenders want to ensure that you have a steady source of income and that you will be able to make your mortgage payments on time.

As a contract employee, you may face some challenges in proving job stability compared to someone with a traditional full-time job. Lenders typically prefer borrowers who have a stable employment history with a consistent income stream. However, this doesn’t mean that it’s impossible for contract employees to get a home loan.

One way to demonstrate job stability is by having a long-term contract with a reputable company. If you have been working for the same company for several years and have a history of renewing your contract, it can help strengthen your case with lenders. Additionally, having a high-demand skill set or working in an industry with a strong job market can also work in your favor.

Another factor that lenders may consider is the length of your contract. If you have a long-term contract, such as a two-year contract, it can provide more reassurance to lenders compared to a short-term contract. Lenders want to see that you have a stable income source for the foreseeable future.

It’s also important to have a contingency plan in case your contract ends or is not renewed. Lenders may want to see that you have savings or other sources of income that can cover your mortgage payments in case of job loss. This can help alleviate concerns about job stability.

Overall, while job stability can be a challenge for contract employees when applying for a home loan, it’s not impossible. By demonstrating a long-term contract, having a stable employment history, and having a contingency plan, you can increase your chances of getting approved for a home loan.

Credit History

When it comes to getting a home loan as a contract employee, your credit history plays a crucial role. Lenders will carefully examine your credit report to assess your financial responsibility and determine your creditworthiness.

A strong credit history is essential for securing a home loan. It demonstrates to lenders that you have a track record of managing your finances responsibly and making timely payments. On the other hand, a poor credit history can make it difficult to qualify for a loan or result in higher interest rates.

If you have a limited credit history or a low credit score, it’s important to take steps to improve your credit before applying for a home loan. This can include paying off outstanding debts, making all payments on time, and keeping credit card balances low.

Additionally, lenders may also consider other factors such as your debt-to-income ratio and employment history when evaluating your creditworthiness. It’s important to provide documentation that demonstrates your ability to repay the loan, such as bank statements, tax returns, and proof of income.

While having a strong credit history is important, it’s not the only factor lenders consider. If you have a solid employment history, stable income, and can provide sufficient documentation to support your loan application, you may still be able to qualify for a home loan as a contract employee.

It’s important to shop around and compare loan options from different lenders to find the best terms and rates for your situation. Working with a mortgage broker or loan officer who specializes in working with contract employees can also be beneficial, as they will have a better understanding of the unique challenges and opportunities you may face.

Exploring the Options

When it comes to getting a home loan as a contract employee, there are several options to consider. While it may be more challenging to secure a loan compared to a traditional employee, it is not impossible. Here are some options to explore:

- Bank Statement Loans: Some lenders offer bank statement loans, which allow contract employees to use their bank statements as proof of income. This can be beneficial for those who have a fluctuating income or do not receive regular pay stubs.

- Portfolio Loans: Portfolio loans are offered by certain lenders who keep the loans on their own books instead of selling them to investors. These loans are often more flexible and can be a good option for contract employees who may not meet the strict requirements of traditional loans.

- Co-Signer: Another option is to have a co-signer with a stable income and good credit history. This can help strengthen the loan application and increase the chances of approval.

- Government-backed Loans: Government-backed loans, such as FHA loans, can also be an option for contract employees. These loans have less stringent requirements and may be more accessible for those with non-traditional employment.

It is important for contract employees to explore these options and work with a knowledgeable lender who understands their unique situation. By doing so, they can increase their chances of obtaining a home loan and achieve their dream of homeownership.

FHA Loans

FHA loans, or Federal Housing Administration loans, are a popular option for contract employees who are looking to secure a home loan. These loans are backed by the government and offer several benefits that make them attractive to individuals with non-traditional employment.

One of the main advantages of FHA loans is that they have more flexible income requirements compared to conventional loans. While traditional lenders may require a steady and consistent income, FHA loans take into account the fluctuating income that contract employees often experience. This means that even if your income varies from month to month, you may still be eligible for an FHA loan.

Another benefit of FHA loans is that they require a lower down payment compared to conventional loans. This can be particularly helpful for contract employees who may not have a large amount of savings. With an FHA loan, you may be able to secure financing with a down payment as low as 3.5% of the purchase price.

In addition to the lower down payment requirement, FHA loans also have more lenient credit score requirements. While traditional lenders may require a higher credit score, FHA loans are available to individuals with lower credit scores. This can be beneficial for contract employees who may have a limited credit history or a lower credit score due to their non-traditional employment.

It’s important to note that while FHA loans offer many advantages, they also have some limitations. For example, there are limits on the amount you can borrow with an FHA loan, which may restrict your options if you’re looking to purchase a more expensive property. Additionally, FHA loans require mortgage insurance, which can increase your monthly payments.

Overall, FHA loans can be a great option for contract employees who are looking to secure a home loan. They offer more flexibility in terms of income requirements, lower down payment options, and more lenient credit score requirements. However, it’s important to carefully consider the limitations and potential costs associated with FHA loans before making a decision.

Question-answer:

Can a contract employee qualify for a home loan?

Yes, a contract employee can qualify for a home loan. Lenders typically consider a variety of factors when determining loan eligibility, including income stability, credit history, and debt-to-income ratio. While being a contract employee may present some challenges, it is still possible to secure a home loan.

What are the requirements for a contract employee to get a home loan?

The requirements for a contract employee to get a home loan are similar to those for regular employees. Lenders will typically look at factors such as income stability, credit history, and debt-to-income ratio. It is important for contract employees to provide documentation of their income, such as tax returns and contracts, to demonstrate their ability to repay the loan.

Are there any specific challenges that contract employees may face when applying for a home loan?

Yes, contract employees may face some challenges when applying for a home loan. One of the main challenges is the lack of a stable income. Lenders typically prefer borrowers with a steady job history and consistent income. Additionally, contract employees may have difficulty providing the necessary documentation to prove their income, as their earnings may vary from month to month.

What can contract employees do to improve their chances of getting a home loan?

Contract employees can take several steps to improve their chances of getting a home loan. Firstly, they can work on building a strong credit history by making timely payments on their existing debts. Secondly, they can save up for a larger down payment, which can help offset any concerns about their income stability. Lastly, contract employees can provide additional documentation, such as letters of recommendation or proof of a long-term contract, to demonstrate their reliability and income potential.

Are there any alternative options for contract employees who are unable to qualify for a traditional home loan?

Yes, there are alternative options for contract employees who are unable to qualify for a traditional home loan. One option is to consider a rent-to-own agreement, where a portion of the monthly rent goes towards building equity in the property. Another option is to explore government-backed loan programs, such as FHA loans, which may have more flexible requirements for contract employees. It is also worth considering working with a mortgage broker who specializes in helping contract employees find suitable loan options.