- What is an IOU Contract?

- Understanding the Basics

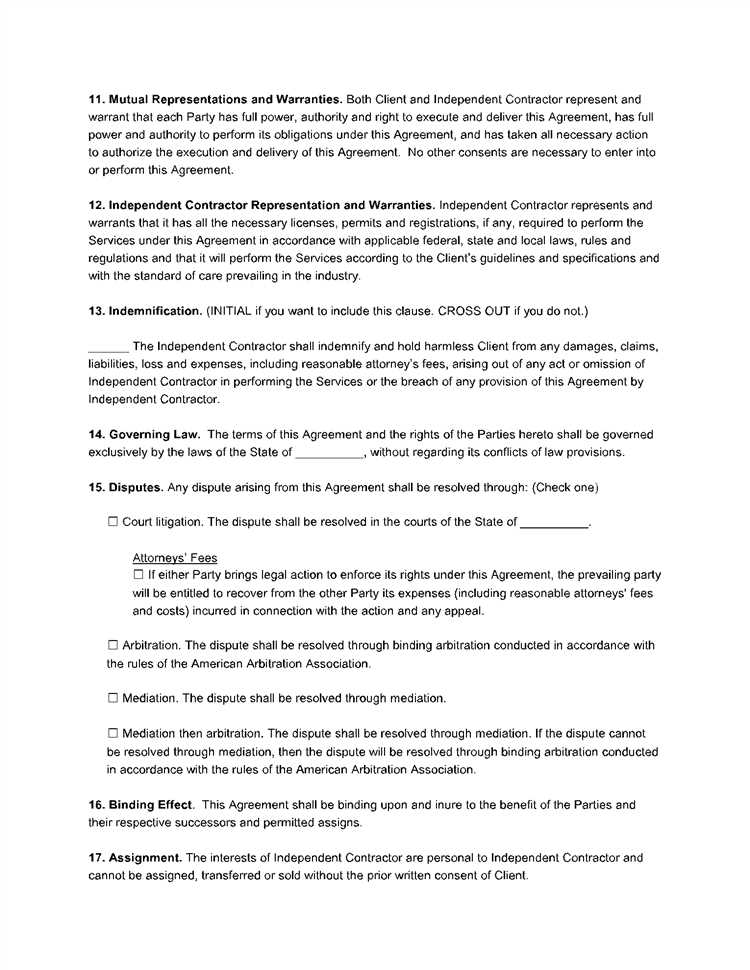

- Legal Considerations

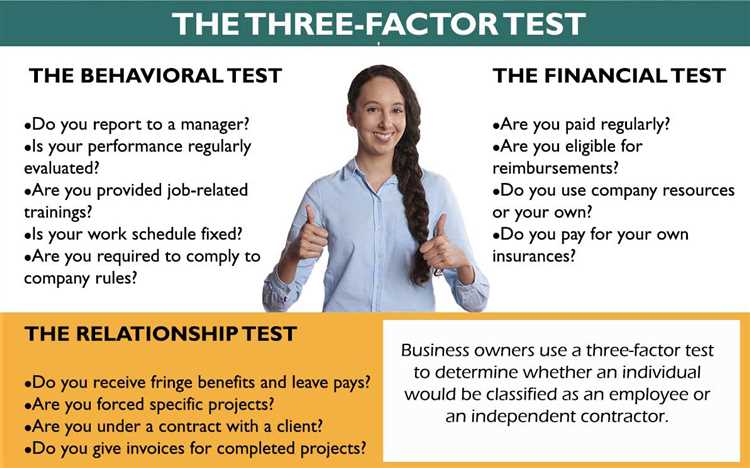

- Can You Use an IOU Contract for Employees?

- Pros and Cons

- Pros:

- Cons:

- Question-answer:

- What is an IOU contract?

- Why would an employer give an employee an IOU contract?

- Is an IOU contract legally binding?

- What happens if an employer fails to fulfill an IOU contract?

- Are there any risks for employees in accepting an IOU contract?

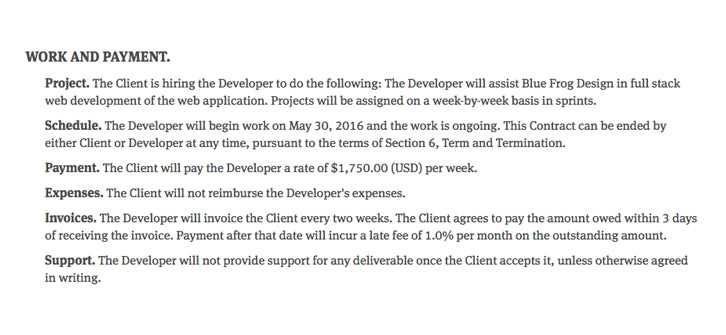

When it comes to employment contracts, there are various types that can be used to outline the terms and conditions of the working relationship between an employer and an employee. One such type is an IOU contract, which stands for “I Owe You.” This type of contract is typically used when an employer is unable to pay an employee their full wages or salary at the time of employment.

An IOU contract is a legally binding agreement that states the employer’s promise to pay the employee the outstanding amount owed at a later date. It is important to note that an IOU contract should only be used in exceptional circumstances, such as when the employer is facing financial difficulties or unexpected cash flow issues.

While an IOU contract can provide a temporary solution for both the employer and the employee, it is crucial to ensure that the terms of the agreement are clearly outlined and agreed upon by both parties. The contract should specify the amount owed, the date by which the payment will be made, and any interest or penalties that may be incurred if the payment is not made on time.

Additionally, it is advisable for both the employer and the employee to seek legal advice before entering into an IOU contract. This will help ensure that the contract is legally enforceable and that both parties understand their rights and obligations. It is also important to keep in mind that an IOU contract should not be used as a long-term solution, and alternative arrangements should be made as soon as possible to ensure the financial stability of both parties involved.

What is an IOU Contract?

An IOU contract, also known as an “I Owe You” contract, is a written agreement between two parties that outlines a debt or obligation. It is a simple and informal way to document a promise to repay a debt or fulfill an obligation without the need for a formal loan agreement or contract.

The IOU contract typically includes the names of the parties involved, the amount owed, the date of the agreement, and any terms or conditions for repayment. It serves as evidence of the debt and can be used as a reference in case of any disputes or misunderstandings.

IOU contracts are commonly used in personal and informal business transactions, such as lending money to a friend or family member, or borrowing money from a colleague. They are often used when the parties involved have a pre-existing relationship and trust each other, but still want to have a written record of the debt.

While IOU contracts are not legally binding in the same way as formal loan agreements, they can still be enforceable in court if both parties agree to the terms and conditions and there is evidence of the debt. However, it is important to note that the enforceability of an IOU contract may vary depending on the jurisdiction and the specific circumstances of the case.

Overall, an IOU contract provides a simple and convenient way to document a debt or obligation between parties without the need for complex legal agreements. It can help maintain transparency and trust in personal and informal business transactions, while still providing some level of legal protection in case of any disputes.

Understanding the Basics

Before diving into the details of an IOU contract, it’s important to understand the basics of what it entails. An IOU contract, also known as an “I Owe You” contract, is a written agreement between two parties that outlines a debt or obligation. It serves as a temporary solution when one party owes money or services to another party.

The IOU contract typically includes important details such as the names of the parties involved, the amount owed, the date of the agreement, and the terms of repayment. It is a legally binding document that can be used as evidence in case of a dispute or non-payment.

IOU contracts are commonly used in personal transactions, such as lending money to a friend or family member, but they can also be used in business settings. For example, if an employer needs to borrow money from an employee, they may enter into an IOU contract to formalize the agreement and establish the terms of repayment.

It’s important to note that an IOU contract is not the same as a promissory note or a formal loan agreement. While a promissory note includes more detailed terms and conditions, an IOU contract is a simpler document that acknowledges the debt and outlines the repayment terms.

IOU contracts can be useful in situations where a formal loan agreement is not necessary or practical. They provide a written record of the debt and can help prevent misunderstandings or disputes between the parties involved.

However, it’s important to consider the potential risks and limitations of using an IOU contract. For example, if the debtor fails to repay the debt as agreed, the creditor may face difficulties in enforcing the contract and recovering the owed amount. Additionally, IOU contracts may not be suitable for larger or more complex transactions that require more comprehensive legal protection.

Legal Considerations

When considering the use of an IOU contract for employees, it is important to understand the legal implications and considerations. While IOU contracts can be a convenient way to handle short-term financial arrangements, there are several legal factors to keep in mind.

Firstly, it is crucial to ensure that the IOU contract complies with all applicable employment laws and regulations. This includes adhering to minimum wage requirements, overtime pay, and other legal obligations. Failure to comply with these laws can result in legal consequences and potential lawsuits.

Additionally, it is important to clearly outline the terms and conditions of the IOU contract. This includes specifying the amount owed, the repayment schedule, and any interest or penalties that may apply. By clearly defining these terms, both parties can avoid misunderstandings or disputes in the future.

Furthermore, it is advisable to consult with a legal professional or employment attorney when drafting an IOU contract for employees. They can provide guidance and ensure that the contract is legally sound and enforceable. This can help protect both the employer and the employee in case of any legal issues or disputes.

Lastly, it is important to keep accurate records of all IOU contracts and payments. This includes documenting the initial agreement, any amendments or changes, and proof of repayment. These records can serve as evidence in case of any disputes or legal proceedings.

| Legal Considerations for IOU Contracts |

|---|

| Compliance with employment laws and regulations |

| Clear and specific terms and conditions |

| Consultation with a legal professional |

| Accurate record-keeping |

Can You Use an IOU Contract for Employees?

When it comes to paying employees, businesses have various options to consider. One option that may come to mind is using an IOU contract. But can you actually use an IOU contract for employees?

An IOU contract, also known as an “I Owe You” contract, is a written agreement between two parties where one party promises to pay a certain amount of money or provide a specific service to the other party at a later date. It is commonly used in informal situations or between friends and family members.

However, when it comes to employees, using an IOU contract may not be the best option. There are several legal considerations to take into account. First and foremost, businesses have a legal obligation to pay their employees for the work they have done. This means that using an IOU contract instead of providing immediate payment may violate labor laws.

Furthermore, using an IOU contract for employees can create a sense of uncertainty and instability in the workplace. Employees rely on their paychecks to cover their living expenses and meet their financial obligations. Delaying payment through an IOU contract can cause financial stress and strain the employer-employee relationship.

Additionally, using an IOU contract for employees may also have tax implications. In many jurisdictions, employers are required to withhold taxes from their employees’ paychecks and remit them to the appropriate tax authorities. Delaying payment through an IOU contract may complicate the tax reporting process and potentially lead to penalties or fines.

Overall, while an IOU contract may be suitable for informal situations, it is not recommended for use with employees. It is important for businesses to fulfill their legal obligations and provide timely payment to their employees. If a business is facing financial difficulties, it is advisable to explore other options such as negotiating payment plans or seeking financial assistance.

Pros and Cons

Using an IOU contract for employees can have both advantages and disadvantages. It is important to carefully consider these pros and cons before deciding to use this type of contract.

Pros:

- Flexibility: An IOU contract can provide flexibility for both the employer and the employee. It allows for a more informal agreement, which can be beneficial in certain situations.

- Informal Nature: IOU contracts are less formal than traditional employment contracts, which can make them easier to create and modify as needed.

- Cost Savings: Using an IOU contract may save the employer money, as it eliminates the need for extensive legal documentation and potentially reduces administrative costs.

- Quick Resolution: In cases where an employee is owed money, an IOU contract can provide a quick and straightforward way to resolve the issue without the need for lengthy legal proceedings.

Cons:

- Lack of Legal Protection: IOU contracts may not offer the same level of legal protection as traditional employment contracts. This can leave both the employer and the employee vulnerable in case of disputes or disagreements.

- Uncertainty: Since IOU contracts are less formal, there may be more uncertainty regarding the terms and conditions of employment. This can lead to misunderstandings and potential conflicts.

- Limited Enforcement: If an employee fails to honor their IOU contract, enforcing the agreement can be challenging. Without the backing of a formal employment contract, legal recourse may be limited.

- Perception: Using IOU contracts for employees may be perceived as unprofessional or lacking commitment by some individuals. This can potentially harm the employer’s reputation and employee morale.

Overall, while IOU contracts can offer flexibility and cost savings, they also come with risks and limitations. It is important to carefully weigh the pros and cons and consider the specific circumstances before deciding to use an IOU contract for employees.

Question-answer:

What is an IOU contract?

An IOU contract is a written agreement between an employer and an employee where the employer promises to pay the employee a certain amount of money at a later date.

Why would an employer give an employee an IOU contract?

An employer may give an employee an IOU contract if they are experiencing temporary financial difficulties and are unable to pay the employee’s salary on time.

Is an IOU contract legally binding?

Yes, an IOU contract is legally binding as long as it meets the requirements of a valid contract, such as offer, acceptance, consideration, and intention to create legal relations.

What happens if an employer fails to fulfill an IOU contract?

If an employer fails to fulfill an IOU contract, the employee may take legal action to enforce the contract and recover the unpaid wages.

Are there any risks for employees in accepting an IOU contract?

Yes, there are risks for employees in accepting an IOU contract. The employer may not be able to fulfill the contract, leading to delayed or unpaid wages. It is important for employees to carefully consider the financial stability of the employer before accepting an IOU contract.