- Understanding the Buyout Process

- Assessing the Property Value

- Determining the Partner’s Share

- Negotiating the Buyout Price

- Financing the Buyout

- Exploring Financing Options

- Applying for a Loan

- Question-answer:

- What is a buyout of a partner on a house?

- Why would someone want to buy out a partner on a house?

- What are the steps involved in buying out a partner on a house?

- How do you determine the value of the property for a buyout?

- What are some potential challenges in buying out a partner on a house?

- What is a buyout of a partner on a house?

- What are the reasons for buying out a partner on a house?

Buying a house with a partner can be an exciting and rewarding experience. However, circumstances may change, and you may find yourself in a situation where you need to buy out your partner’s share of the property. Whether it’s due to a breakup, a change in financial circumstances, or simply a desire to have full ownership, the process of buying out a partner on a house can be complex.

Before you begin the buyout process, it’s important to have a clear understanding of the legal and financial implications involved. You’ll need to consider factors such as the current market value of the property, any outstanding mortgage or loans, and the terms of your partnership agreement, if you have one. It’s also crucial to communicate openly and honestly with your partner about your intentions and expectations.

Once you’ve done your research and had open discussions with your partner, you can begin the step-by-step process of buying out their share of the house. First, you’ll need to determine the value of the property. This can be done through a professional appraisal or by researching recent sales of similar properties in your area. It’s important to be objective and realistic when assessing the value, as this will form the basis for negotiations.

Next, you’ll need to agree on a fair price for your partner’s share of the property. This can be a challenging step, as emotions and differing opinions may come into play. It’s important to approach this negotiation with a calm and rational mindset. Consider factors such as the initial investment, any improvements made to the property, and the current market conditions. It may be helpful to involve a mediator or seek legal advice to ensure a fair and equitable agreement.

Once you’ve reached an agreement on the price, you’ll need to secure financing for the buyout. This may involve refinancing the existing mortgage or obtaining a new loan. It’s important to shop around for the best rates and terms, and to consider the impact of the buyout on your overall financial situation. You may also need to consult with a real estate attorney or financial advisor to navigate the legal and tax implications of the buyout.

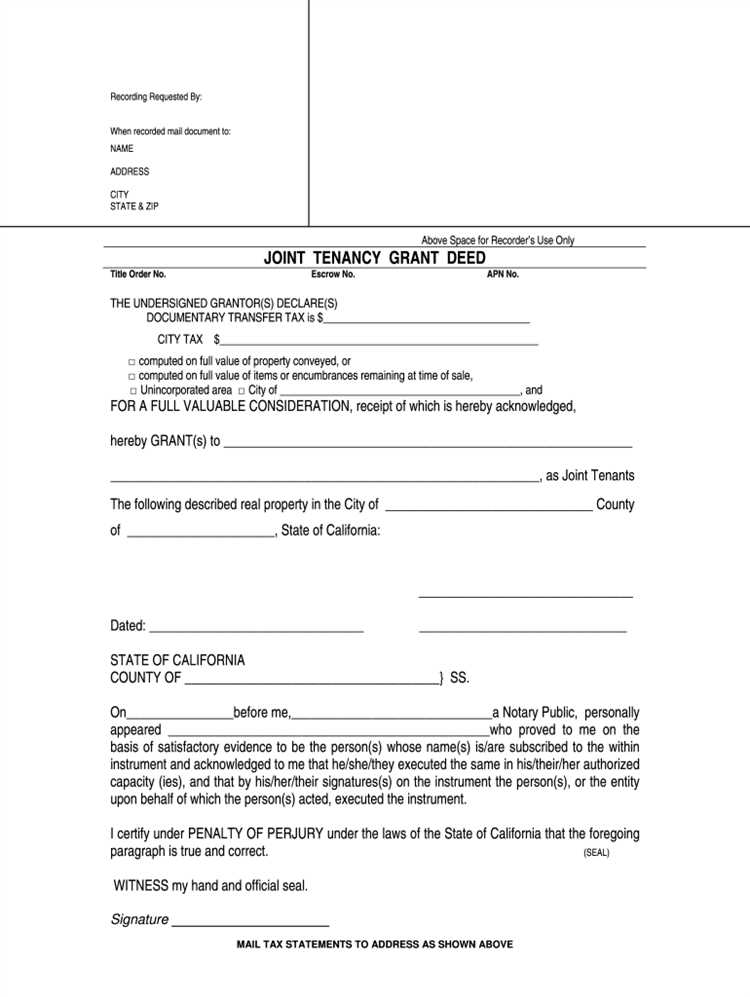

Finally, once the financing is in place, you’ll need to complete the necessary paperwork to transfer ownership of the property. This may involve drafting a new deed, updating the mortgage documents, and notifying relevant parties such as the local government and homeowners’ association. It’s important to follow the proper legal procedures to ensure a smooth and legally binding transfer of ownership.

Buying out a partner on a house can be a complex and emotional process, but with careful planning and open communication, it can be successfully navigated. By following this step-by-step guide, you’ll be well-equipped to handle the financial and legal aspects of the buyout, and to move forward with full ownership of your property.

Understanding the Buyout Process

When it comes to buying out a partner on a house, it is important to understand the process involved. This can help ensure a smooth and successful transaction. Here are some key points to consider:

1. Communication: The first step in the buyout process is open and honest communication between both partners. It is essential to discuss the reasons for the buyout and come to a mutual agreement.

2. Legal Considerations: Before proceeding with the buyout, it is important to consult with a real estate attorney to understand the legal implications. They can guide you through the process and ensure all necessary documents are prepared.

3. Property Appraisal: To determine the fair market value of the property, a professional appraisal is necessary. This will help in determining the buyout price and ensure a fair deal for both parties.

4. Partner’s Share: It is crucial to determine the partner’s share in the property. This can be based on various factors such as initial investment, mortgage payments, and any improvements made to the property.

5. Negotiation: Once the property value and partner’s share are determined, negotiations can begin. Both parties should be open to compromise and work towards a mutually agreeable buyout price.

6. Financing Options: Depending on the financial situation, there are various financing options available for the buyout. This can include obtaining a loan, refinancing the mortgage, or using personal funds.

7. Loan Application: If a loan is required for the buyout, it is important to gather all necessary documents and apply for the loan. This may include income verification, credit history, and property information.

8. Closing the Deal: Once all negotiations and financing are in place, the final step is to close the deal. This involves signing the necessary paperwork, transferring ownership, and ensuring all legal requirements are met.

By understanding the buyout process and following these steps, you can navigate the complexities of buying out a partner on a house successfully. It is always recommended to seek professional advice and guidance throughout the process to ensure a fair and smooth transaction.

Assessing the Property Value

Assessing the property value is a crucial step in the process of buying out a partner on a house. It involves determining the fair market value of the property to ensure a fair and equitable buyout.

There are several methods that can be used to assess the property value:

1. Comparative Market Analysis (CMA): This method involves analyzing recent sales of similar properties in the same area. By comparing the features, size, and condition of the property with others that have recently sold, an estimate of the property’s value can be determined.

2. Appraisal: Hiring a professional appraiser can provide an unbiased and accurate assessment of the property’s value. The appraiser will consider factors such as the property’s location, size, condition, and recent sales of comparable properties to determine its value.

3. Online Valuation Tools: There are various online tools available that can provide an estimate of the property’s value based on publicly available data. While these tools can be a helpful starting point, they should not be relied upon solely as they may not take into account specific features or conditions of the property.

Once the property value has been assessed, it is important to consider any factors that may affect its value, such as any repairs or renovations that may be needed. These factors should be taken into account when determining the buyout price.

It is recommended to consult with a real estate professional or an attorney specializing in real estate transactions to ensure an accurate assessment of the property value and to navigate the buyout process smoothly.

Determining the Partner’s Share

When buying out a partner on a house, it is crucial to determine their share of the property. This step is essential to ensure a fair and equitable buyout process. Here are some factors to consider when determining the partner’s share:

| Factor | Description |

|---|---|

| Initial Investment | Consider the amount each partner initially invested in the property. This includes the down payment, closing costs, and any other expenses related to the purchase. |

| Mortgage Payments | Take into account the mortgage payments made by each partner. This includes both the principal and interest payments over the course of ownership. |

| Property Improvements | Assess any improvements made to the property during the partnership. This can include renovations, repairs, or additions that have increased the value of the house. |

| Market Value | Consider the current market value of the property. This can be determined by conducting a professional appraisal or researching recent sales of similar properties in the area. |

| Agreed-upon Percentage | Partners may have agreed upon a specific percentage of ownership when purchasing the property. This percentage should be taken into account when determining the partner’s share. |

Once all these factors have been considered, you can calculate the partner’s share by adding up their initial investment, mortgage payments, property improvements, and adjusting for the agreed-upon percentage. It is important to involve a professional, such as a real estate attorney or appraiser, to ensure an accurate assessment of the partner’s share.

By determining the partner’s share accurately, you can proceed with the buyout process confidently, knowing that it is fair and equitable for both parties involved.

Negotiating the Buyout Price

When it comes to buying out a partner on a house, negotiating the buyout price is a crucial step in the process. This is the stage where you and your partner will determine the fair value of their share in the property and come to an agreement on the buyout amount.

Here are some key points to consider when negotiating the buyout price:

| 1. Property Appraisal: | It is important to get a professional property appraisal to determine the current market value of the house. This will provide an objective assessment of the property’s worth and serve as a starting point for negotiations. |

| 2. Consideration of Contributions: | Take into account the financial contributions made by each partner towards the purchase and maintenance of the property. This includes the initial down payment, mortgage payments, and any renovations or repairs. These contributions can influence the buyout price. |

| 3. Market Conditions: | Evaluate the current real estate market conditions in your area. If the market is hot and property prices are rising, the buyout price may be higher. Conversely, if the market is slow or declining, the buyout price may be lower. |

| 4. Future Prospects: | Consider the potential future value of the property. If there are plans for development or improvements in the area that could increase the property’s value, this should be taken into account during negotiations. |

| 5. Mediation or Legal Assistance: | If you and your partner are having difficulty reaching an agreement on the buyout price, it may be helpful to involve a mediator or seek legal assistance. They can provide guidance and help facilitate a fair negotiation process. |

Remember, the goal of negotiating the buyout price is to reach a fair and mutually acceptable agreement. It is important to approach the process with open communication, transparency, and a willingness to compromise. By considering the factors mentioned above and seeking professional advice if needed, you can navigate the negotiation process successfully and secure a fair buyout price for both parties involved.

Financing the Buyout

Once you have determined the buyout price and agreed upon it with your partner, the next step is to figure out how to finance the buyout. There are several financing options available to consider:

- Personal Savings: If you have enough savings, you can use your own funds to finance the buyout. This option allows you to avoid taking on additional debt and interest payments.

- Home Equity Loan: If you have built up equity in your home, you can consider taking out a home equity loan to finance the buyout. This type of loan allows you to borrow against the value of your home and use the funds for the buyout.

- Mortgage Refinancing: Another option is to refinance your existing mortgage and take out additional funds to finance the buyout. This can be a good option if you can secure a lower interest rate or if you need to extend the repayment period.

- Personal Loan: You can also explore the option of taking out a personal loan to finance the buyout. This type of loan is unsecured, meaning you don’t need to use your home or any other asset as collateral.

- Partnership Buyout Loan: Some lenders offer specific loans designed for partnership buyouts. These loans are tailored to meet the needs of individuals who are buying out their partners and often come with favorable terms and conditions.

Before deciding on a financing option, it’s important to carefully consider your financial situation, including your income, credit score, and existing debts. You should also shop around and compare different lenders to find the best terms and interest rates.

Once you have chosen a financing option, you will need to apply for the loan. This typically involves providing the lender with documentation such as proof of income, bank statements, and a copy of the buyout agreement. The lender will review your application and make a decision on whether to approve the loan.

Once the loan is approved, you can use the funds to complete the buyout and transfer ownership of the property solely to yourself. It’s important to keep in mind that taking on additional debt to finance the buyout will increase your monthly expenses, so make sure you can comfortably afford the loan payments before proceeding.

Exploring Financing Options

When it comes to buying out a partner on a house, financing the buyout can be a major consideration. There are several financing options available that can help you fund the buyout and make the process smoother.

One option is to obtain a traditional mortgage loan. This involves applying for a loan from a bank or mortgage lender to cover the cost of buying out your partner’s share. The advantage of this option is that you can spread out the payments over a longer period of time, making it more manageable for your budget.

Another option is to consider a home equity loan or line of credit. If you have built up equity in the property, you can use it as collateral to secure a loan. This can be a good option if you have a good credit score and can qualify for a favorable interest rate.

If you don’t qualify for a traditional mortgage or home equity loan, you may want to explore alternative financing options. For example, you could consider a personal loan from a bank or online lender. Keep in mind that the interest rates on personal loans can be higher, so it’s important to carefully consider the terms and conditions before proceeding.

Additionally, you may want to explore the possibility of borrowing from friends or family members. This can be a more flexible option, as you can negotiate the terms and repayment schedule directly with your loved ones. However, it’s important to approach this option with caution and ensure that both parties are comfortable with the arrangement.

Before making a decision, it’s important to carefully evaluate your financial situation and consider the long-term implications of each financing option. Take the time to compare interest rates, loan terms, and repayment schedules to find the option that best suits your needs and budget.

| Financing Option | Advantages | Disadvantages |

|---|---|---|

| Traditional Mortgage Loan | Spread out payments over a longer period of time | Requires a good credit score and may have strict eligibility criteria |

| Home Equity Loan or Line of Credit | Can use built-up equity as collateral | Interest rates may vary and require good credit |

| Personal Loan | Can be obtained from banks or online lenders | Interest rates may be higher and repayment terms may be shorter |

| Borrowing from Friends or Family | Flexible terms and repayment schedule | May strain personal relationships if not handled carefully |

Remember, it’s important to consult with a financial advisor or mortgage professional to fully understand the implications of each financing option and make an informed decision. By exploring the various financing options available, you can find the best solution to buy out your partner on a house and move forward with your homeownership goals.

Applying for a Loan

Once you have determined the buyout price and explored financing options, it’s time to apply for a loan to finance the buyout of your partner on the house. Here are the steps to follow:

1. Research Lenders: Start by researching different lenders and their loan products. Look for lenders who specialize in home buyout loans or have experience in financing real estate transactions. Compare interest rates, terms, and fees to find the best option for your situation.

2. Gather Documentation: Lenders will require various documents to process your loan application. These may include proof of income, tax returns, bank statements, and information about the property. Gather all the necessary documentation to speed up the application process.

3. Complete the Loan Application: Fill out the loan application form provided by the lender. Provide accurate and detailed information about your financial situation, the property, and the buyout price. Double-check the application for any errors before submitting it.

4. Submit the Application: Submit the completed loan application along with the required documentation to the lender. Some lenders may allow you to submit the application online, while others may require you to visit their office in person. Follow the lender’s instructions for submission.

5. Wait for Approval: After submitting the application, you will need to wait for the lender to review and process it. This may take a few days to a few weeks, depending on the lender’s workload. Be patient during this time and avoid making any major financial decisions.

6. Provide Additional Information: During the loan processing, the lender may request additional information or documentation. Be prepared to provide any requested information promptly to avoid delays in the approval process.

7. Review the Loan Offer: Once the lender has reviewed your application, they will provide you with a loan offer. Carefully review the terms and conditions, including the interest rate, repayment period, and any fees associated with the loan. If you have any questions or concerns, don’t hesitate to ask the lender for clarification.

8. Accept the Loan Offer: If you are satisfied with the loan offer, sign the loan agreement to accept it. Make sure you understand all the terms and conditions before signing. Keep a copy of the agreement for your records.

9. Close the Loan: After accepting the loan offer, the lender will guide you through the closing process. This involves signing the final loan documents and transferring the funds to complete the buyout of your partner on the house. Follow the lender’s instructions and provide any additional documentation or information as required.

10. Repay the Loan: Once the loan is closed, you will need to start making regular payments according to the agreed-upon terms. Set up automatic payments if possible to ensure timely repayment and avoid any penalties or late fees.

By following these steps and carefully navigating the loan application process, you can successfully finance the buyout of your partner on the house and take full ownership of the property.

Question-answer:

What is a buyout of a partner on a house?

A buyout of a partner on a house refers to the process of one person buying out the ownership share of another person in a jointly owned property.

Why would someone want to buy out a partner on a house?

There are several reasons why someone may want to buy out a partner on a house. It could be due to a change in financial circumstances, a desire to have full control over the property, or a breakdown in the partnership.

What are the steps involved in buying out a partner on a house?

The steps involved in buying out a partner on a house typically include assessing the value of the property, negotiating a buyout price, obtaining financing if necessary, drafting a buyout agreement, and completing the necessary legal and financial paperwork.

How do you determine the value of the property for a buyout?

The value of the property for a buyout can be determined through various methods, such as hiring a professional appraiser, researching recent sales of similar properties in the area, or using online valuation tools.

What are some potential challenges in buying out a partner on a house?

Some potential challenges in buying out a partner on a house include disagreements over the value of the property, difficulties in obtaining financing, and navigating the legal and financial aspects of the buyout process.

What is a buyout of a partner on a house?

A buyout of a partner on a house is a process where one co-owner of a property purchases the ownership interest of another co-owner, allowing them to become the sole owner of the property.

What are the reasons for buying out a partner on a house?

There can be several reasons for buying out a partner on a house. Some common reasons include a change in personal circumstances, such as a divorce or a breakup of a business partnership, or a desire to have full control and ownership of the property.